Lawyer. I have been practicing law since 2017. Currently, I have my own law firm, where I am a managing partner. I mainly deal with disputes with the tax office, accompany inspections. I run enterprises from 0 and full support of economic activity. Consultations on any issues. Currently, I also have practice in military affairs.

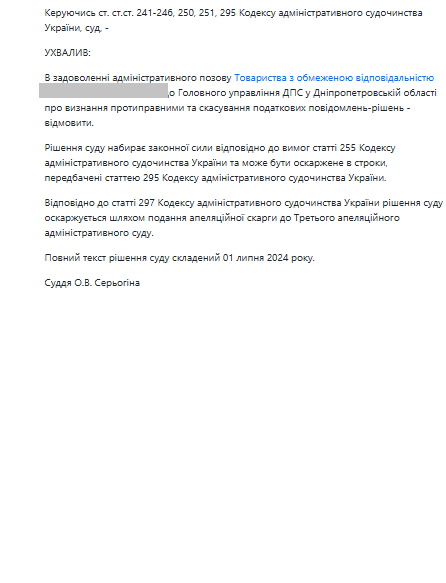

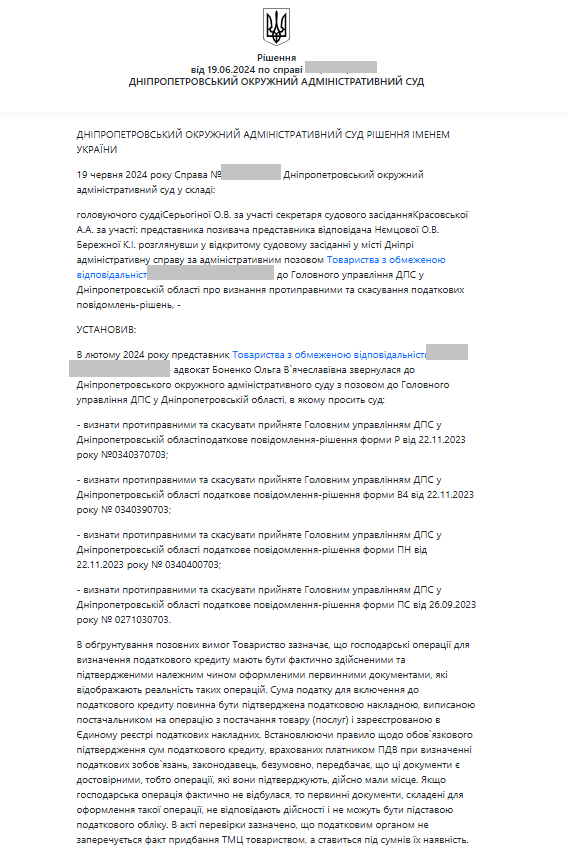

Case Summary: Cancellation of tax notices issued following an audit in which the tax authority questioned the reality of business transactions and the existence of inventory.

Responsible Attorney:

Olha Vyacheslavivna Niemtsova

Case Details:

In early 2024, a business client contacted our law firm after the tax authority imposed tax liabilities amounting to millions of hryvnias. The issue arose following an unscheduled on-site audit during which the tax authority denied the existence of inventory that had been included in the VAT credit calculation.

The audit was triggered by the client’s declared negative VAT value exceeding UAH 100,000. During the audit, the tax authority initiated an inventory check to confirm the actual availability of goods. The company issued an order to conduct the inventory and began it in the presence of tax officers. However, without explanation, the inspectors terminated the inventory process and refused to continue or provide a copy of the inventory act. Meanwhile, the tax authority stated in the audit report that inventory worth over UAH 26 million was not confirmed, using this as a basis to issue four tax notices.

Although all primary documents were properly executed and VAT invoices registered in the Unified Register, the tax authority questioned the validity of the VAT credit, without proving that the business transactions were fictitious or unreal.

Result:

The attorney prepared a comprehensive claim to the Dnipro District Administrative Court, demanding recognition of the tax authority’s actions as unlawful and cancellation of all four tax notices. The claim argued that:

- The business transactions were real and supported by documentation;

- All VAT invoices were duly registered by the suppliers;

- The tax authority had no grounds to request documents unrelated to the audit of the negative VAT for June 2023;

- The audit was conducted with procedural violations, and the inventory check was not properly completed due to the tax authority’s own actions.

After correcting formal deficiencies, the court opened proceedings and scheduled a preparatory hearing. The tax authority submitted a written response, again focusing on the lack of inventory documents but failing to dispute the validity of registered VAT invoices or the authenticity of primary accounting records.

Legal Basis:

The attorney referred to the provisions of the Tax Code of Ukraine, particularly subparagraph 78.1.8 of Article 78, as well as Supreme Court case law, which states that minor errors in primary documents or the absence of certain certificates cannot be grounds for denying a VAT credit if the reality of the transaction is not disproved.

Subparagraph 78.1.8 of Paragraph 78.1, Article 78 of the Tax Code of Ukraine provides the tax authority with the right to conduct an unscheduled documentary audit if it receives tax information indicating possible violations of tax legislation that cannot be verified through cross-checks, or if the taxpayer fails to provide the requested explanations or documents within the established timeframe.

Attorney’s Actions:

- Analysis of the audit report and tax authority requests:

Assessed the content of the documents and identified overreach by the tax authority.

- Evidence gathering and legal strategy:

The attorney compiled a detailed set of documents confirming the actual supply and accounting of goods.

- Drafting and filing the claim:

The claim provided strong legal arguments proving the illegality of the tax authority’s actions, particularly regarding the inventory process.

- Legal representation in court:

The attorney represented the client at all stages, from case initiation to analysis of the tax authority’s response.

This case clearly demonstrates that even in the presence of an audit report with significant tax assessments, competent legal representation enables effective protection of business interests in court.

Attorney Olha Vyacheslavivna Niemtsova not only built a legally flawless case but also showed professional resilience in confronting a tax authority that effectively manipulated the procedure to achieve fiscal objectives.